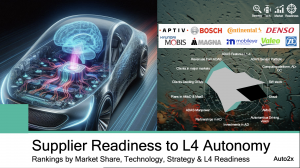

The report evaluates major suppliers based on Technology Competitiveness, Strategy Execution & Market Positioning. Learn about new opportunities and challenges.

— Auto2x

LONDON, UNITED KINGDOM, August 24, 2024 /EINPresswire.com/ — Competition among Suppliers in ADAS and Autonomous Driving is getting stronger.

Auto2x has released its “Suppliers Readiness in Level 4 Autonomous Driving Rankings” report, offering unparalleled insights into the evolution of the competitive landscape of Advanced Driver Assistance Systems (ADAS) and the roadmaps to Level 4 autonomous driving of technology providers.

– Learn about suppliers’ capabilities of suppliers in sensors, features, computing and software to deliver Level 1-4 cruising and parking.

– Understand the strategies and technologies to realise their vision, including partnerships, investments, M&A, new product launches, supply chain and business models.

– Get insights on who is better positioned in the marketplace, their revenues from ADAS and how new entrants will shape competition.

The rankings cover the Top-20 ADAS Tier-1s, including APTIV, Bosch, Continental, Denso, Mobileye, Valeo, and ZF, in addition to Baidu, Alibaba, Amazon, Huawei, Foxconn and others.

Key findings from the Auto2x 2024 Ranking of Supplier Readiness in Level 4 Autonomous Driving.

– Incumbent Tier-1 suppliers lead the ADAS market, but they face challenges to transform and fight the competition

– Emerging Chinese Suppliers and tech entrants threaten the leadership of major Tier-1s in ADAS & Electrification

– New opportunities in perception, computing, AI, SDVs and new markets

– Suppliers should continue investing in tech, strengthen partnerships and build customer-centric business models

Who Should Read This Report:

– Automotive OEMs and Tier 1-2 Suppliers

– Technology companies exploring automotive market entry

– Investors and financial analysts focused on the automotive sector

– Automotive industry consultants and strategists

How Readers Will Benefit:

– Gain a comprehensive understanding of the current ADAS supplier landscape

– Identify potential partners or acquisition targets for autonomous driving technology

– Assess competitive threats from both established players and new entrants

– Guide strategic decision-making around R&D investments and market positioning

– Understand emerging trends and technologies shaping the future of autonomous driving

1. Which suppliers are better prepared for the new era of Autonomous Mobility?

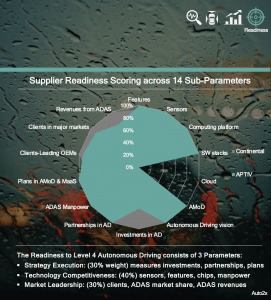

Auto2x assessed the readiness levels of major Tier-1 suppliers and emerging players based on their technological competitiveness, their strategy execution and their market positioning.

• The first parameter, Technology Competitiveness, captures the product portfolio of sensors, features, architecture, software stack and innovation (patents).

Auto2x assesses that APTIV and Continental have high readiness levels in Level 4 Autonomous Driving Technology due to their mature offering in Lidar, Software stack and Computing Platforms.

• Strategy Execution, the 2nd parameter, covers a supplier’s partnerships, investments, ADAS manpower, activities in autonomous mobility and more.

Bosch and Mobileye lead the pack in this parameter, with strong in-house capabilities, a partner ecosystem in high-growth areas and investments in key markets.

Continental is a 100% system supplier from design and manufacturing to validation and expansion to new services in system integration and functions. This makes them well-positioned.

• Market Positioning, the 3rd parameter, captures the volume of ADAS revenues from sensors and features, sensor market share, client base and geographical presence.

2. Major Automotive Tier-1 Suppliers like Bosch, ZF, Valeo, Denso and Continental still maintain the lion’s share in terms of automotive revenues.

Furthermore, their revenues from ADAS, electrification and new mobility business models are increasing. ADAS revenues from the Top-12 Suppliers rose by 12.5% in 2021 y-y to €16 Billion. Auto2x expects it will double by 2025 to €35 Billion.

Continental led the ADAS market by revenues between 2015 and 2018, mainly by capitalising on its dominance in the camera market.

But they were overtaken by Bosch in 2019, who leads the market by ADAS revenues since then. The contracts with OEMs for ADAS and the ability to support driving and parking features for higher levels of automation are strengths.

• Overall Readiness Level: The Ranking of Suppliers Readiness in Autonomous Driving is based on their competence in three parameters, Strategy (30% weight), Technology (40%) and Market Position (30%).

Auto2x found that Bosch leads the ADAS market by revenues from sensors for Level 1-2 features, but they lag in Technology Readiness for Level 4 Autonomous Driving.

Another success story is Mobileye which spearheads INTEL’s Autonomous Driving strategy and has captured a large share in ADAS. Mobileye ranks at the Top3 of Auto2x’s Ranking of Suppliers by Readiness in level-4 Automated Driving.

European suppliers lead the race. ZF and Continental broke the €2 Billion mark in ADAS revenues, but challenges remain

The Top-4 Automotive Suppliers of ADAS are all European, Bosch, Valeo, ZF and Continental, according to Global ADAS Ranking by Revenues. The 4% growth in automotive production in 2022 and the higher sensor fitment for Level 2-3 systems benefited their ADAS sales and Order Books.

• ZF achieved 33% growth in ADAS revenues in 2022 to €2.4 Billion, from €1.8B in 2021. ZF ranked 3rd in the Global ADAS Ranking by Revenues in 2021 from Auto2x with an 11% market share.

• Continental saw 23% growth in ADAS sales to €2.1 Billion in 2022, from €1.7B in 2021. ADAS accounted for 11% of Continental’s Automotive revenues.

But major automotive suppliers face further transformation to develop capabilities in AI and software, expand into software business models and face new competition

3. What risks do leading Automotive ADAS Suppliers face?

Suppliers face risks from increased competition, particularly from tech giants and emerging players that leverage AI and cloud technologies, potentially disrupting traditional supply chains.

The transformation of carmakers into mobility service providers pressures suppliers to adapt quickly to software-driven models, which may require significant investment and restructuring.

Additionally, the shift from hardware to software monetization poses challenges for suppliers reliant on traditional revenue streams, necessitating an evaluation of their business strategies to remain competitive.

4. How could new suppliers and Tech Giants disrupt major Tier-1s?

Traditional ADAS suppliers still maintain the lion’s share in automotive supplier revenues. But they face competition from US, Chinese and other Tech giants who capitalize on their expertise in AI, Cloud and Software transforming automotive.

We have identified several opportunities for Tech Companies to enter or disrupt the existing supply chain.

• Next-gen Perception Hardware for Autonomous Driving:

• Computing, e.g. Peta-ops chips for Autonomous Driving

The computing power required for a

– Lv.2 vehicle is 10 TOPS (tera operations per second),

– Lv.4 exceeds 100 TOPS,

– Lv.5 vehicle will require a 1,000 TOPS computing processing power.

• AI: AI for Autonomy and HMI such as in-car AI assistants

• Data-based Business models such as in-car e-commerce

• 5G-6G, Connected Infrastructure and Smart Cities

• Autonomous Shared Mobility and autonomous deliveries

Mobileye spearheads INTEL’s Autonomous Driving strategy and has captured a large share in ADAS. Baidu offers competitive technology due to Apollo’s strengths.

5. What challenges do automotive companies face in achieving Level 4 autonomy?

Automotive companies face several challenges in achieving Level 4 autonomy, including the need for advanced sensor technology and high-performance computing platforms to process vast amounts of data in real-time.

Regulatory hurdles and safety standards must be navigated to ensure compliance and public acceptance of autonomous vehicles.

Significant investments in research, development, and partnerships are required to build the necessary infrastructure and technology ecosystem for successful deployment.

6. New opportunities in SDV for Connected and Autonomous Driving

Software-on-Wheels revolution will determine Mobility’s future

Electrification, automated driving, shared mobility and connectivity push for more dedicated software development. A large part of hardware-oriented systems becomes more standardized and commoditized.

The growing number of ECUs with sophisticated software leads to significant cost increases, higher in-vehicle software complexity and constraints in optimising vehicular functions.

Next-generation Digital vehicles must integrate new, diverse technologies and complex logical operations; the hardware architecture has to support advanced software functionality and upgradability.

New partnerships and new business models are emerging.

What are some key new Software-driven features with high potential?

Software is the answer to the Digitization of the Automotive Industry but delivery is challenging. Learn about top innovation clusters across major technological building blocks of SDVs.

• EE Architectures: Assess the roadmaps of leading carmakers and suppliers in the development of centralized architectures and their partnerships;

o Aptiv’s Active Safety Domain Controller integrated by BMW,

o Visteon’s Domain Controller SmartCore, launched by Mercedes Benz;

o one-oriented control units (ZCUs), where the vehicle is divided into zones and each zone integrates into a zone-ECU (the sub-ECUs do not perform any processing to realize a vehicle function)

e.g. Bosch’s zone-oriented E/E architecture;

o and cross-domain centralized units (CDCUs), where the functions of more than one domain are consolidated onto a single ECU (similar to the DCU’s architecture)- e.g. Bosch’s vehicle-centralized ECU.

• CarOS: Learn about the rising adoption of Google’s Android Automotive OS and the competitive offerings from MBUX and other players;

• Open-source software development

• Cloud: the emergence of automotive cloud as an enabler for cloud-based ADAS development, development of offerings from carmakers and the role of Microsoft, Amazon among others;

• Over-the-Air-updates and the opportunities for features-on-demand;

• Digital Twin

7. How could innovation in AI and cloud computing impact autonomous driving?

New technologies like AI and cloud computing are crucial for the future of autonomous driving as they enable advanced data processing, real-time decision-making, and scalable software updates.

AI enhances vehicle perception and autonomy through machine learning and in-car assistants, while cloud computing supports efficient feature development and system integration.

Together, they facilitate the transition to higher levels of automation and improve overall vehicle performance and safety.

The integration of AI and cloud computing will change the consumer experience in autonomous vehicles

The integration of AI and cloud computing will significantly enhance the consumer experience in autonomous vehicles by enabling personalized in-car services, such as tailored entertainment and real-time navigation assistance.

Cloud computing allows for continuous updates and feature enhancements, ensuring vehicles remain up-to-date with the latest technology and safety features.

Additionally, AI-powered virtual assistants can provide seamless interaction, improving convenience and overall satisfaction during travel

8. How can Suppliers stay competitive and gain competitive advantage?

What should suppliers do to stay relevant in autonomous driving, gain competitive advantage and market share?

Suppliers should invest in next-generation technologies, such as advanced perception hardware, AI, cloud computing to meet the evolving demands of autonomous driving.

Another important aspect is building competence in Autonomous Driving software and sensors needed by carmakers to develop higher autonomy.

Huawei supplies LIDAR and car networking to BAIC for L2+. Huawei has recently launched new products in Autonomous Driving focusing on ADAS sensors (4D imaging radar), HMI (AR-HUD) during their product launch titled ‘Focused Innovation for Intelligent Vehicles’.

Samsung Electronics will work together with Tesla to develop chips for their HW 4.0;

They should also adapt their strategies to identify new revenue pools and collaborate with innovative partners to tap into high-growth opportunities.

By forming commercial and product development partnerships with volume carmakers to support their connected, electric and ADAS roadmaps. The AI and connectivity domains in the booming Chinese market are particularly crucial for new AD Suppliers to claim market share from global Tier1s

Additionally, suppliers must continuously assess competition and enhance their product offerings to maintain a competitive edge in the market.

Finally, fuel investments in innovative technologies and business models incl. robotaxis, and last-mile delivery.

9. Recommendations for new market entrants

What are some key market entry strategies for new suppliers? Which technologies show potential for them to enter and which countries?

Key market entry strategies for new suppliers include forming strategic partnerships with established players, investing in innovative technologies, and focusing on niche markets within the autonomous driving sector.

Technologies with potential for entry include next-gen perception hardware, AI for autonomy, and advanced computing solutions.

Countries with promising opportunities for new suppliers include China, the USA, and regions in Europe, where demand for autonomous driving solutions is rapidly growing.

The “ADAS Suppliers Rankings” report is available now through Auto2x’s website. For more information or to schedule an interview with our analysts.

Mariola Skoczynska

Auto2x LTD

+ +447426975395

email us here

Visit us on social media:

LinkedIn

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Article originally published on www.einpresswire.com as Auto2x ranks Automotive Suppliers by Readiness in Level 4 Autonomous Driving